Cash-on-Cash Return

Explore how effectively your investment cash is generating income in a rental property. Our Cash-on-Cash Return guide provides easy definitions and formulas, real-world examples, and actionable strategies to boost your returns through smart improvements, financing techniques, and tax planning.

Cash-on-Cash Return

Cash-on-cash return (CoC) measures the annual pre-tax cash flow from a rental property relative to the amount of cash you invested. This calculation focuses solely on your out-of-pocket contribution and the actual money you’re receiving back each year. It’s a vital tool for comparing leveraged properties, especially when different down payments, financing terms, and cash flows are involved.

KEY TAKEAWAYS

- Focus on Actual Cash: Cash-on-cash return evaluates how effectively your invested cash is generating cash flow, making it a more practical metric for leveraged properties than ROI or cap rate. It focuses solely on what you’ve put into the deal and what you’re getting out of it each year, in terms of real cash.

- Pre-Tax Perspective: CoC considers only annual pre-tax cash flow, excluding appreciation, tax benefits, or principal paydown. This means it provides a clean and simple measure of operational cash performance.

- Compare Investment Deals: It enables investors to compare multiple deals on a cash-in vs. cash-out basis, especially useful when analyzing properties with different financing structures, renovation requirements, or market locations.

- Boost Through Strategy: You can significantly improve CoC by raising rents, reducing expenses, using creative financing (like seller carrybacks or interest-only loans), or applying tax strategies such as accelerated depreciation or cost segregation studies.

- Ideal for New Investors: CoC is easy to calculate and interpret, making it ideal for beginners assessing day-one cash flow potential. It’s a great first filter before diving into more complex ROI metrics.

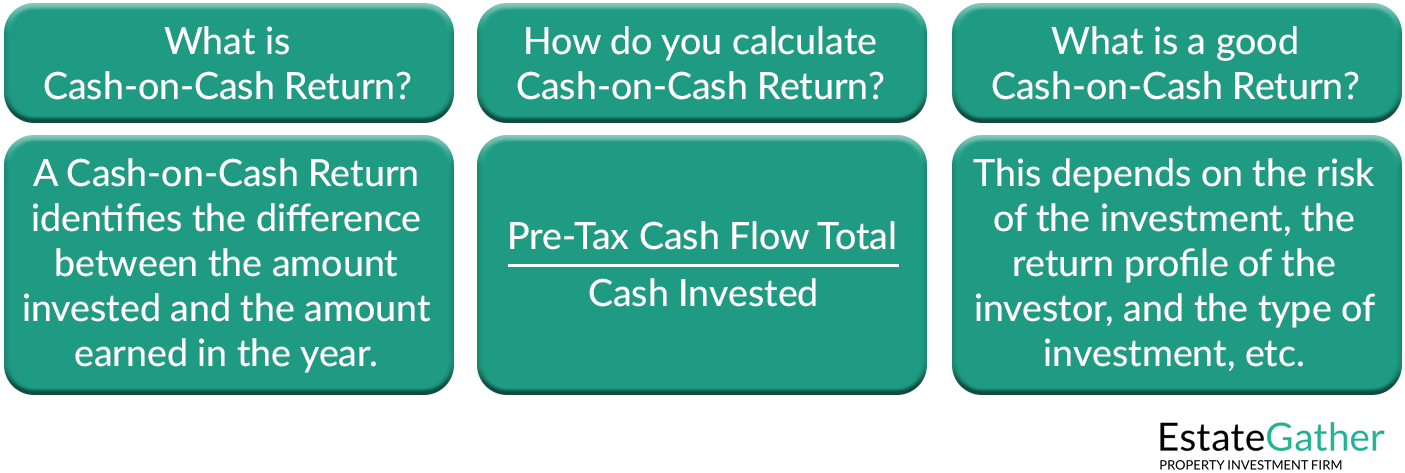

What is Cash-on-Cash Return?

Cash-on-cash return (CoC) is a simple metric that measures the annual cash flow from a real estate investment relative to the initial cash you put into the deal. In other words, it tells you how much cash profit you’re earning each year as a percentage of the cash you invested. This metric focuses only on actual cash invested (your out-of-pocket money) and the actual cash generated from rents after operating expenses. CoC is especially useful for rental properties financed with loans, because it isolates your cash earnings on the equity you’ve invested, excluding the loan amount. It’s one of the first figures many investors look at to gauge a rental’s cash flow performance and to compare different investment opportunities on an “apples to apples” cash basis.

Why it Matters

A strong CoC return means your property is putting cash back in your pocket relatively quickly. For example, a CoC of 10% indicates that each year you’re earning back 10% of the cash you invested (through the property’s net cash flow). Many investors consider an 8-12% CoC a good range, with anything above 12% being excellent in most markets. A higher CoC generally implies a shorter payback period on your initial cash and a more cash-efficient investment. On the flip side, a low CoC (say 2-4%) might occur in expensive markets or with properties that have slimmer cash flow – it signals that your money is yielding a smaller immediate return. Keep in mind that CoC is a snapshot of cash flow; it doesn’t account for other benefits like appreciation, loan paydown, or tax advantages. So while CoC is a critical metric for cash flow-focused investors, it should be considered alongside other measures (like cap rate, IRR, etc.) for a full picture of an investment’s performance.

Sponsor

YOUR

ADVERTISEMENT

HERE

Just $20 a Month, for full site coverage.

How to Calculate Cash-on-Cash Return

Calculating CoC return is straightforward. The formula is:

Cash-on-Cash Return = (Annual Pre-Tax Cash Flow ÷ Total Cash Invested) × 100%

- Determine Annual Cash Flow: Calculate the property’s yearly net cash flow before taxes. This is typically the rent income minus all operating expenses and minus any debt service (mortgage payments). For example, if the property brings in $15,000 in rent per year and expenses (including mortgage) total $12,000, the annual pre-tax cash flow is $3,000.

- Determine Total Cash Invested: Add up all the cash you’ve put into the property. This includes your down payment, closing costs, and any upfront renovation or furnishing costs. For instance, if you put $40,000 down on the property, paid $5,000 in closing costs, and spent $5,000 on initial repairs, your total cash invested is $50,000.

- Apply the Formula: Divide the annual cash flow by the total cash invested, then multiply by 100 to get a percentage. Using the numbers above, CoC = ($3,000 / $50,000) × 100 = 6%. This means you’re earning a 6% return on the cash you put into the property from the cash flow alone.

This calculation gives a quick gauge of cash profitability. A higher CoC percentage means a better cash return on your investment. For example, if another property yields $5,000 annual cash flow on the same $50,000 cash invested, its CoC would be 10%, which is more attractive. Remember, CoC uses pre-tax cash flow and doesn’t include non-cash expenses like depreciation. It’s all about the cash in vs. cash out on an annual basis.

Example: Long-Term Rental

Let’s walk through a detailed example for a long-term rental (traditional year-long lease to tenants). Suppose you buy a single-family rental house with the following details:

- Property Purchase Price: $200,000

- Down Payment (25%): $50,000 (this is your equity in the property)

- Closing Costs: $5,000 (loan fees, title, etc., also your cash out of pocket)

- Upfront Repairs: $5,000 (minor fixes to get the home rent-ready)

Your total cash invested is $50,000 + $5,000 + $5,000 = $60,000.

Now let’s project the annual cash flow:

- Monthly Rent: $1,500 (tenant pays all utilities)

- Annual Gross Rent: $1,500 × 12 = $18,000

- Operating Expenses: Let’s estimate $8,000 for the year (this includes property taxes, insurance, maintenance, and a bit set aside for vacancies).

- Net Operating Income (NOI): $18,000 – $8,000 = $10,000 (income before mortgage payments)

- Annual Debt Service: $150,000 loan at 6% interest for 30 years has a payment of about $900 per month, which is $10,800 per year (covering principal and interest).

- Annual Pre-Tax Cash Flow: NOI $10,000 – Mortgage $10,800 = –$800.

In this scenario, the property is actually slightly cash flow negative (losing $800/year) primarily due to the mortgage cost. That would yield a negative CoC return, which is obviously not ideal (you’d be feeding the property a bit of cash). This can happen with lower-yield properties or in high-cost markets.

Let’s adjust the scenario to achieve a positive cash flow: imagine you were able to buy the same property at a lower price or higher rent. Say the annual NOI is $12,000 and the annual mortgage is still $10,800. Then the annual cash flow is $1,200. Now:

- Cash-on-Cash Return: $1,200 / $60,000 = 0.02 = 2% CoC.

A 2% CoC is quite low – this might be typical for a property in an expensive coastal city where rents barely cover the mortgage. If instead the rent was higher and produced, for example, $5,000 in annual cash flow, then:

- CoC Return: $5,000 / $60,000 = 8.3% CoC.

Now we’re talking – about an 8% return on cash, which falls into a “good” range for many investors. This long-term rental example shows how CoC reflects your cash flow yield. Small changes in rent or expenses (or the financing terms) can make a big difference in your CoC. As an investor, you’d run these numbers before buying to ensure the property meets your target return. Many buy-and-hold rental investors aim for something like an 8-10% CoC if possible, but what’s “good” can depend on your strategy and market.

Sponsor

YOUR

ADVERTISEMENT

HERE

Just $20 a Month, for full site coverage.

Example: Short-Term Rental

For a contrasting scenario, let’s calculate CoC on a short-term rental, such as an Airbnb vacation home. Short-term rentals often have higher income potential but also different costs. Here’s our scenario:

- Property: 3-bedroom vacation cabin – Purchase Price: $300,000.

- Down Payment (10% second-home loan): $30,000 (many vacation rental loans allow lower down payments).

- Closing Costs: $5,000.

- Furniture & Setup Costs: $20,000 (short-term rentals must be furnished and equipped).

Total Cash Invested: $30,000 + $5,000 + $20,000 = $55,000.

Now, the income side: As a short-term rental, income is calculated nightly rather than monthly, and it can fluctuate with seasons and occupancy rates.

- Average Nightly Rate: $200 (this will vary, but let’s assume an average booking rate of $200/night).

- Occupancy Rate: 60% (on average the cabin is rented about 18 nights per month).

From this, we can estimate Gross Annual Rent: $200 × 18 nights × 12 months = $43,200 per year.

Short-term rentals incur a variety of expenses, often higher (as a percentage of income) than long-term rentals:

- Cleaning & Supplies: $5,000 per year (you or your manager pay for cleaning between guests, toiletry restocks, etc.).

- Utilities & Wi-Fi: $3,000 per year (you cover all utilities for a vacation rental).

- Maintenance & Repairs: $2,500 (guests can be tough on a property, so this covers wear-and-tear fixes).

- Property Management: $8,600 per year (many owners use a management service or give a 20% cut; 20% of $43,200 = $8,640).

- Property Taxes & Insurance: $4,000 (often similar to a long-term rental’s taxes/insurance).

Adding those up, total annual operating expenses come to roughly $23,100. Subtract that from the $43,200 gross rent to get NOI: about $20,100.

Now consider the mortgage. We financed 90% of $300K, so the loan is $270,000. At, say, a 6% interest rate (30-year term), the annual mortgage payments are about $19,400.

- Annual Pre-Tax Cash Flow: NOI $20,100 – Mortgage $19,400 ≈ $700.

This particular set of assumptions yields only a small positive cash flow ($700 for the year). If that were the case, the CoC Return is modest: $700 / $55,000 ≈ 1.3%. But short-term rental performance can vary widely. Let’s tweak the scenario to see a stronger outcome – perhaps our occupancy or nightly rates were underestimated:

Suppose the cabin actually averages 70% occupancy at $220/night thanks to a great location and marketing. Then:

- Gross Annual Rent: $220 × 21 nights × 12 = ~$55,440.

- Keeping expenses proportional (they might rise a bit with more occupancy, but let’s estimate operating expenses now at $27,000 – higher cleaning and utilities with more stays). NOI: $55,440 – $27,000 = $28,440.

- Annual Pre-Tax Cash Flow: $28,440 – $19,400 (mortgage) = $9,040.

Now CoC = $9,040 / $55,000 ≈ 16.4%. That’s a much higher return on cash! This illustrates why investors are attracted to short-term rentals – the income can be significantly more than a traditional lease, potentially driving CoC into double digits. In our adjusted scenario, a ~16% CoC is well above average. Of course, it comes with trade-offs: managing a short-term rental is more hands-on (or involves higher management fees), income can be seasonal, and there may be local regulations affecting Airbnb-type properties. But from a pure numbers standpoint, a successful short-term rental can deliver a strong cash-on-cash return compared to many long-term rentals.

Note: When analyzing CoC for any property, make sure to include all the cash you must invest. For short-term rentals, that means furniture, supplies, and sometimes higher closing costs or insurance. Those upfront costs should be counted in your “cash invested,” which will temper the CoC a bit. In our example, if we hadn’t included the $20K furnishing in the investment, the CoC would look higher – but that would be an oversight since furnishing is a real cash outlay. Always do a realistic accounting of your cash investment and your net cash flow.

Sponsor

YOUR

ADVERTISEMENT

HERE

Just $20 a Month, for full site coverage.

Maximizing Cash-on-Cash Return

Once you understand your CoC, the next step is figuring out how to improve it. Whether your current CoC is 4% or 14%, there are strategic ways to boost that return. Essentially, you can either increase the property’s cash flow or decrease the amount of cash you have tied up in the deal (or both). Below are several investor strategies – all beginner-friendly – to optimize cash-on-cash returns:

- Increase Rental Income with Smart Improvements: One of the most direct ways to raise CoC is to increase the property’s NOI (net operating income). Higher rent or additional income streams mean more cash flow, which boosts CoC. You can often charge higher rent by adding desirable amenities or upgrades. For instance, including an in-unit washer/dryer can justify a rent increase – landlords can typically command around a $50 higher monthly rent when offering in-unit laundry, which can pay for the appliance in under a year. Similarly, updating the kitchen or bathroom can allow you to ask more rent or attract better tenants. Quality renovations tend to pay off: kitchen and bath remodels often recoup an estimated 60-85% of their cost in increased value or rent potential. Even simple cosmetic improvements like fresh paint, new lighting, or adding covered parking can let you bump the rent a bit. The key is to focus on improvements with high ROI. If spending $5,000 on upgrades can increase your annual rent by $1,000 (for example, ~$80 more per month), that’s a 20% return on the upgrade cost – and your property becomes more competitive in the market, potentially reducing vacancy. Always research your local market to see which amenities renters will pay premium for (it might be a dishwasher, air conditioning, or extra storage space). By strategically boosting income, you directly improve your CoC since more cash flow on the same investment yields a higher percentage return.

- Lower Your Expenses (and thus Increase NOI): Another side of improving NOI is cutting unnecessary costs. While you can’t remove major expenses like property taxes, you might reduce others. Shop around for cheaper insurance or install energy-efficient fixtures to cut utility bills if you pay them. Preventive maintenance can reduce big repair bills down the line. If you’re paying high property management fees, you might negotiate a better rate or even self-manage if it’s feasible – saving 8-10% on management could substantially increase your cash flow. Every dollar saved in expenses is a dollar added to your annual cash flow, improving your CoC return. Just be careful not to under-maintain the property; short-term savings shouldn’t lead to long-term damage. The goal is efficient management: operate the property leanly without compromising tenant satisfaction or the home’s condition.

- Use Creative Financing to Reduce Upfront Cash: CoC can dramatically improve if you reduce your initial cash outlay. The less of your own cash you have tied up in the deal, the higher your return on that cash (for a given amount of cash flow). One way to do this is through high-leverage or creative financing:

- Higher LTV Loans: If you finance more of the purchase (i.e. a smaller down payment), your cash invested is lower. Certain loan products cater to investors and allow lower downs – for example, some DSCR loans (Debt Service Coverage Ratio loans, popular for rental investors) offer 85-90% financing, meaning you only put 10-15% down. Using more of the lender’s money can “significantly improve cash-on-cash returns” because you’re amplifying returns on a smaller equity stake. Note: Higher leverage will increase your mortgage payments, so you must ensure the property still cash flows well.

- Interest-Only Loans: With an interest-only mortgage, you pay only interest (no principal) for an initial period. This keeps monthly payments lower in those early years, boosting your cash flow. More cash flow with the same investment means a better CoC. Investors might use interest-only loans when cash flow is tight in the beginning – say during a property stabilization period – to improve their CoC until rents can be raised. It’s a trade-off since you’re not building equity during the interest-only phase, but it can be a useful strategy to maximize cash returns upfront.

- Seller Financing & Other Creative Deals: In some cases, the property seller might finance part of the deal (a seller carry-back note), or you can get a second loan to cover part of the down payment. For example, a seller might let you buy a property with only 10% down by “carrying” an extra 10% as a second mortgage. In that scenario, your cash invested is only 10%, which could double your CoC return compared to a standard 20% down deal (since you’ve halved the cash investment). Seller financing can also mean below-market interest rates or deferred payments. These arrangements are less common, but when they happen, they increase CoC by lowering the cash required from you. Anytime you’re leveraging other people’s money on favorable terms, your cash-on-cash metric will benefit – just be sure the deal’s overall numbers (and risks) still make sense.

- Strategic Tax Planning (Boost After-Tax Cash Flow): Taxes might not show up directly in the basic CoC formula, but they have a big effect on how much cash you actually keep from your investment. Smart tax strategies can indirectly improve your CoC by increasing your post-tax cash flow (or by giving you cash back at tax time). One powerful tool for rental property owners is cost segregation with accelerated depreciation. Cost segregation is a tax strategy where you categorize portions of the property (e.g. appliances, fixtures, landscaping) into shorter depreciation lifespans (5, 7, or 15 years instead of the standard 27.5 years for residential real estate). By front-loading more depreciation in the early years, you can take larger tax deductions early on. This often creates a paper loss or significantly lowers your taxable rental income, meaning you pay less in taxes those first several years. The immediate result is more cash in your pocket now – effectively boosting your cash flow. For example, if depreciation and other write-offs reduce your taxable rental income to zero, you might pay no taxes on that $10,000 of cash flow you earned – saving perhaps a couple thousand dollars in taxes, which is cash you retain. Those tax savings make your effective cash-on-cash return higher than the nominal pre-tax figure. Accelerated depreciation (including bonus depreciation tactics when available) can be complex, so it’s wise to work with a CPA or tax advisor familiar with real estate. Additionally, strategies like using a LLC and business deductions, writing off home-office or auto expenses related to your rentals, or utilizing a 1031 exchange upon sale to defer taxes can all help you keep more cash. The bottom line: tax planning can greatly enhance investment cash flow. Every dollar not paid in tax is a dollar of return you keep. Just be mindful that some benefits (like depreciation) might be recaptured or taxed later, but in the meantime you enjoy improved cash flow which boosts your short-term CoC results.

- Target High-Yield Markets: Not all real estate markets are created equal when it comes to cash-on-cash returns. Some regions, especially in the Midwest and parts of the South, have lower property prices relative to rents – which is a recipe for higher CoC returns (these are often called “cash flow markets”). In contrast, many coastal cities (think California or New York) have very high purchase prices but only moderately higher rents, resulting in low or even negative CoC in the early years. Choosing the right market can drastically improve your chances of a strong CoC. Broadly speaking, the best cash flow opportunities tend to be in places like Texas, the Midwest, and the Southeast, whereas the West Coast and expensive Northeast cities offer little in terms of immediate cash flow. For example, buying a $120,000 duplex in Cleveland, OH that rents for $1,200 per month per unit could generate a double-digit CoC, which might be hard to achieve on a $800,000 single-family in Los Angeles. Investors looking for high CoC often focus on areas with affordable home prices and steady rental demand – cities with stable or growing economies but where real estate hasn’t boomed so much that rents lag far behind prices. These might include parts of the Midwest (Ohio, Michigan, Indiana, Missouri), the Southeast (parts of Florida, Alabama, Georgia), or pockets of the Southwest and Texas. By acquiring properties in these high rent-to-price ratio markets, your rent cash flow is high relative to the cash needed to buy in. Data supports this approach: one analysis found that many of the top U.S. markets for cash flow in 2024 were in states like Texas and Missouri, while expensive coastal markets had the lowest yields. Of course, there are trade-offs – high-CoC markets may have slower property appreciation or different management challenges (e.g. older housing stock). And even in low-CoC areas, you can sometimes find individual deals that buck the trend. The key is market research. If maximizing cash-on-cash is your goal, direct your search toward investor-friendly locales known for better rent-to-value ratios. Sometimes the best approach is a balanced one: for instance, some investors in pricey coastal cities choose to purchase their rental investments long-distance in high-yield midwestern towns to get that great cash flow, while their home equity in the coastal city builds wealth via appreciation. Decide what mix of cash flow vs. appreciation you want, and plan your market strategy accordingly.

By applying some or all of the above strategies, even a newbie investor can meaningfully boost their cash-on-cash returns. For instance, imagine you bought a rental townhouse that initially had a 5% CoC. You add coin-operated laundry machines in the basement for extra income and raise rents a bit after a minor kitchen update – increasing annual cash flow. You also refinance the property to an interest-only loan for five years, slashing your monthly payment. Meanwhile, a cost segregation study at tax time wipes out most of your taxable rental income, so you owe very little tax on that cash flow. Individually, each move might bump your CoC a few percentage points; combined, you might turn that 5% into 10-12% (hypothetically). Every property and market will differ, but the overarching lesson is CoC return is not fixed – you can actively manage and improve it. This is part of the fun of real estate investing: through savvy upgrades, financial restructuring, and market choices, you have levers to pull that can maximize the cash returns on your investment.

Conclusion: Cash-on-cash return is one of the most important metrics for rental property analysis, especially for those seeking passive income. It tells you, in plain percentage terms, how hard your invested cash is working for you each year. As a new investor, focus on learning to calculate CoC and understanding what drives it. Use it to compare deals and to identify where you can optimize. Just remember to view it in context – a high CoC is fantastic, but not if it comes with untenable risk or neglects the bigger investment picture (appreciation, equity buildup, etc.). Combine CoC with other metrics and a sound strategy. By doing so, you’ll be well on your way to making informed, financially rewarding real estate investments. Happy investing!

Frequently Asked Questions (FAQ)

What is a good cash-on-cash return for a rental property?

A “good” CoC return is typically between 8% and 12%, though it varies by market, risk tolerance, and investment goals. Higher returns (12%+) are common in cash-flow-heavy markets like the Midwest or Southeast, while lower returns (4–6%) may be acceptable in high-appreciation areas.

How is cash-on-cash return different from ROI or cap rate?

Cash-on-cash return only considers the annual pre-tax cash flow relative to your actual cash invested. ROI (Return on Investment) includes appreciation and loan paydown, and cap rate uses NOI divided by purchase price, ignoring financing. CoC is most useful for leveraged properties.

Can cash-on-cash return be negative?

Yes. If your property’s net cash flow is negative (due to high expenses, low rent, or a large mortgage), the CoC will also be negative. This indicates your investment is losing cash annually and should be evaluated carefully.

Does cash-on-cash return include taxes or depreciation?

No, CoC is a pre-tax metric. It doesn’t include depreciation, tax deductions, or tax credits. However, smart tax planning (like cost segregation or accelerated depreciation) can increase your after-tax cash flow, effectively improving your return.

How can I improve my cash-on-cash return?

You can increase CoC by:

- Targeting high rent-to-price ratio markets

- Raising rents through value-add improvements

- Reducing expenses (e.g., insurance, management fees)

- Using creative or low down-payment financing

- Applying tax strategies to lower taxable income

Is CoC relevant for short-term rentals like Airbnb?

Absolutely. CoC can be even more important for short-term rentals because of their high income potential and startup costs (furnishings, supplies, cleaning). Just be sure to include all upfront cash expenses in your calculation.

Should I use CoC alone to decide on an investment?

No. CoC is best used alongside other metrics such as internal rate of return (IRR), cap rate, and ROI. A high CoC might indicate strong cash flow, but it doesn’t capture long-term equity growth, tax efficiency, or risk factors.

How often should I recalculate my cash-on-cash return?

Recalculate your CoC annually or whenever major changes occur—such as rent increases, refinancing, or significant renovations. Tracking it over time helps you measure your property’s cash performance and spot trends.

What expenses should I include when calculating total cash invested?

Include your down payment, closing costs, initial repairs, furnishings (if applicable), loan fees, and any other upfront cash outlays. Don’t include financed amounts or recurring operating costs.

Is CoC useful for BRRRR or Live-In-Then-Rent strategies?

Yes. In fact, these strategies often produce excellent CoC returns because of low upfront costs and forced appreciation. After refinancing or moving out, you may have very little cash left in the deal—drastically improving your CoC.